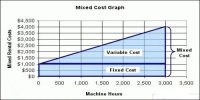

Incremental cost can be defined as the encompassing changes experienced by a company within its balance sheet because of tint additional unit of production. It is the increase in total costs resulting from an increase in production or other activity. This is also referred to as ‘marginal cost’. However, the incremental cost cannot always be the same as the average cost per unit due to different (Fixed and Variable) costs involved. Moreover, the incremental cost is always made up of purely variable costs. It characterizes the added costs that might not exist it an extra unit was not produced. It is calculated by analyzing the additional charges incurred based on the change in a certain activity.

For example, if a company’s total costs increase from $320,000 to $360,000 as the result of increasing its machine hours from 8,000 to 10,000, the incremental cost of the 2,000 machine hours is $40,000.

Sometimes incremental cost is also called as a marginal cost because marginal cost is nothing but the increase in cost due to the increase per one unit of product.