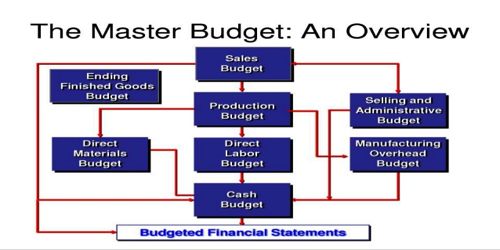

Muster budget is a summary of a company’s plan that sets specific targets for sales, production, financial activities and that generally achieves in a cash budget, budgeted income statement and budgeted balance sheet. It is the aggregation of all lower-level budgets produced by a company’s various functional areas, and also includes budgeted financial statements, cash forecast, and a financing plan. It is normally presented in both a monthly or quarterly system, and generally covers a company’s whole fiscal year. It is the summary of the divisional budget. It is a continuous financial plan.

Contents of the master budget: The main components of a master budget include income and expenses, and production costs, and the monthly, annual, and average totals. The major contents are as follows –

- Sales budget,

- Production budget,

- Direct material budget,

- Direct labor budget,

- Factory overhead budget,

- Variable costs of the production budget,

- Operating expenses budget,

- Cash receipt budgets,

- Cash payment budget,

- Cash budget,

- The variable cost of goods of the sold budget,

- Budgeted income statement,

- Budgeted balance sheet.