Monopolistic competition is a form of imperfect competition where many competing producers sell products that are differentiated from one another. In monopolistic in the short run including using market power to generate profit. In the long run, other firms enter the market and the benefits of differentiation decreases with competition; the market becomes more like a perfect competition where firms cannot gain economic profit.

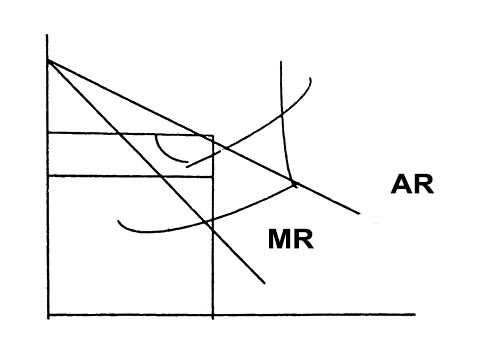

Short run equilibrium of the firm under monopolist competition. The lire maximize it’s profit and produces a quantity where the firm’s marginal revenue (MR) is equal to its marginal cost (MC). The firm is able to collect a price based on the average revenue (AR) curve. The difference between the firms average revenue and average cost gives it a profit.