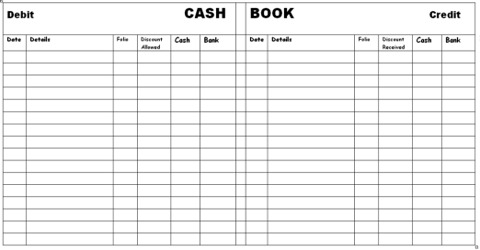

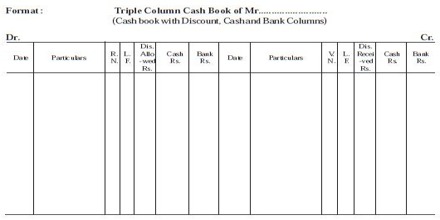

A three column cash book or treble column cash book is one in which there are three columns on each side – debit and credit side. One is used to record cash transactions, the second is used to record bank transactions and third is used to record discount received and paid.

Postings from Triple Column Cash Book to concerned ledger accounts

- Opening (Cash and Bank) balance appearing in the cash book is not posted to an account in the ledger. The opening balances of cash book are not posted.

- Contra entries are not posted to an account. Contra entries are not posted because the double entry accounting for these transactions is accomplished within the cash book.

- Each item of discount allowed appearing on the debit side of the cash book will be posted to the credit of the respective personal account. Total of discount allowed column should be posted to the debit side of discount allowed account with the words “To Sundry Accounts”.

- Each item of discount received appearing on the credit side of the cash book will be posted to the debit of respective personal account. Total of discount received column should be posted to the credit of discount received account with the words “By Sundry Accounts”.

- The other transactions recorded on the debit side of the cash book are posted to the credit of the respective accounts in the ledger.

- The other transaction recorded on the credit side of the cash book is posted to the debit of the respective accounts in the ledger.