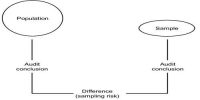

Audit Procedure for obtaining Audit Evidence

Audit Procedures are specific acts performed as the auditor gathers evidence to determine if specific assertions are beignet. They are used by auditors to determine the quality of the financial information being provided by their clients.

Audit evidence which is cumulative in nature includes audit evidence obtained from audit procedures performed during the course of the audit and may include audit evidence obtained from other sources such as previous audits and a firm’s quality control procedures for client acceptance and continuance.

Audit procedure for obtaining audit evidence: Audit procedure for obtaining audit evidence is given below-

(a) Inspection of records or documents,

(b) Inspection of tangible assets,

(c) Re-performance,

(d) Re-calculation,

(e) Scanning,

(f) Inquiry,

(g) Observation,

(h) Confirmation,

9i) Analytical procedure.