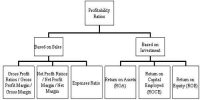

Limitations of Managerial Accounting

The main objective of management accounting is to help internal management. It focuses on the present and forecasts for the future. Though management accounting is helpful tool to the management as it provides information for planning, controlling and decision making, still its effectiveness is limited by a number of reasons. Some of the limitations of management accounting are as follows:

Based On Accounting Information

Management accounting is based on data and information provided by financial accounting and cost accounting. If the past data is not reliable, the decisions suggested by management accountant may be misleading. As such the correctness and effectiveness of managerial decisions will depend upon the quality of data provided by cost and financial accounts.

Lack Of Knowledge

Deficiency in knowledge in related subjects like accounting principles, statistics, economics, principle of management etc. will limit the use of management accounting. But it has been observed that the person who is taking the decisions may not have comprehensive knowledge of all such subjects.

Intensive Decisions

Decision making based on management accounting that provides scientific analysis of various situations will be time-consuming one. As such management may avoid systematic procedures for taking decision and arrive at decision using intuitively.

Management Accounting Is Only A Tool

The tools and techniques of management accounting provide only information and not decisions. The actual decisions, their implementation, and follow up action are the prerogative of the management. Decisions are to be taken by the management and implementations of decisions are also done by management.

Evolutionary Stage

Management accounting is still in a development stage and has not yet reached a final stage. The techniques and tools used by this system give varying and differing results. That is why its techniques suffer from fluidity of concepts, diversity in opinions and various interpretations.

Personal Prejudices And Bias

The interpretation of financial information may differ from person to person depending upon the capability of the interpreter. Analysis and interpretation of data and information may be influenced by personal basis.

Psychological Resistance

Changes in traditional accounting practices and organizational set up are required to install the management accounting system. These changes are resisted by the management itself as it creates difficulties in its successful operations.