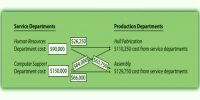

The basis of Apportionment of Overheads

Cost allocation is the assigning of a common cost to several cost objects. For example, a company might allocate or assign the cost of an expensive computer system to the three main areas of the company that uses the system. A company with only one electric meter might allocate the electricity bill to several departments in the company.

Apportionment is an allocation based on some proportions associate the term apportionment with a corporation’s taxable income that was earned in many states within the U.S. In that situation, the Corporation’s taxable income must be allocated or apportioned to each of the states based upon certain accepted factors. In the past, the apportionment or allocation was often based on a corporation’s tangible property, employees, and sales in each of the states. More recently, apportionments seem to be based more on sales or receipts within each state.

A managerial accounting cost method of expensing all costs associated with manufacturing a particular product. Absorption costing uses the total direct costs and overhead costs associated with manufacturing a product as the cost base. Generally accepted accounting principles (GAAP) require absorption costing for external reporting.

Following are the main bases of overhead apportionment utilized in manufacturing concerns:

(i) Direct Allocation: Overheads are directly allocated to various departments on the basis of expenses for each department respectively.

(ii) Direct Labor/Machine Hours: Under this basis, the overhead expenses are distributed to various departments in the ratio of a total number of labor.

(iii) Direct Wages: This method is used only for those items of expenses which are booked with the amounts of wages.

(v) Number of Workers: This method is used for the apportionment of certain expenses as welfare and recreation expenses, medical expenses, timekeeping, supervision etc.

(vi) Technical Estimates: This basis of apportionment is used for the apportionment of those expenses for which it is difficult, to find out any other basis of apportionment.