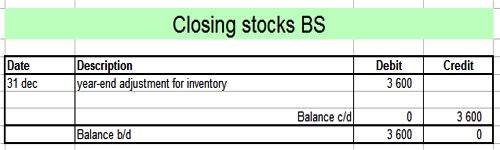

Closing stock means the worth of goods which are remain unsold in an exacting accounting period. It is the amount of inventory that a business still has on hand at the end of a reporting period. This includes raw materials, work-in-process, and finished goods inventory. The amount of closing stock can be ascertained with a substantial count of the inventory. It can also be indomitable by using a permanent inventory method and cycle counting to frequently regulate inventory records to arrive at ending balances.

The closing sock may be in the appearance of raw materials, work in progress or finished goods. It is valued at cost or market price. The amount of closing stock (properly valued) is used to arrive at the cost of goods sold in a periodic inventory system with the following calculation:

Opening stock + Purchases – Closing stock = Cost of goods sold

The opening stock for the next accounting period is the same as the closing stock from the straight away earlier period.