Opening Entry

When a business begins the books for a new year, it has to make what is known as the opening entry in the journal. Opening Entry is an entry which is passed in the beginning of each existing year to record the closing balance of assets and liabilities of the preceding year.

In this entry asset accounts are debited and liabilities and capital account are credited. If capital is not given in the question, it will be found out by subtracting total of liabilities from entire of assets.

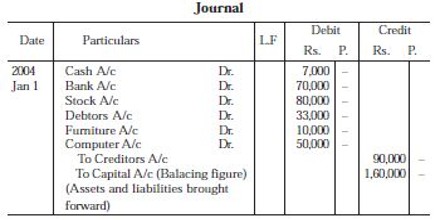

Example: The following balances appeared in the books of Malarkodi as on 1st January 2004 – Cash Rs. 7,000, Bank Rs.70,000, Stock Rs.80,000, Furniture Rs.10,000, Computer Rs.50,000, Debtors Rs.33,000 and Creditors Rs.90,000.

The opening entry is

Advantages

The major advantages of the Journal are:

- It reduces the chance of errors.

- It makes available a clarification of the transaction.

- It makes available a sequential record of all transactions.

Limitations

The boundaries of the Journal are:

- It will be lengthy if all transactions are recorded here.

- It is hard to determine the balance of every account.