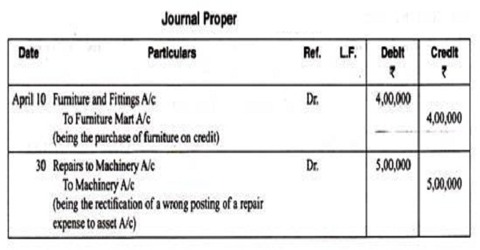

Journal Proper

Journal Proper is mostly used for unique records of a transaction which due to their significance or rareness of incidence do not find a place in any of the supplementary books of accounting. It is used for assembly the unique record of such transactions for which no particular journal has been reserved in the business. The use of this book is very much restricted in modern accounting system. The usual entries that are put through this journal are explained below.

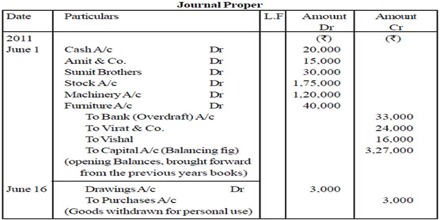

Opening Entries: Opening entries are used at the start of the financial year to open the books by recording the assets, liabilities and capital appearing in the balance sheet of the previous year.

Closing Entries: Closing entries are recorded at the end of the accounting year for closing accounts relating to operating expense and revenues. These accounts are stopped by transferring the balances to the Trading, Profit and Loss Account.

Adjusting Entries: To arrive at a correct figure for profits and loss, certain accounts require some adjustments. Entries for making such adjustments are called as adjusting entries. These are needed at the time of preparing the final accounts.

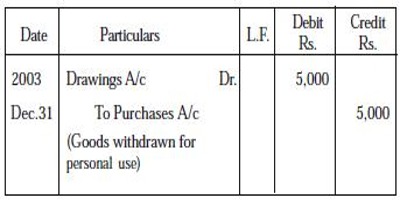

Transfer Entries: In simple terms, the transfer entry is used to transfer an item from one account into another. All such transfers are made with the help of journal entries.

Example: When the proprietor takes goods Rs.5,000 for personal use. Give transfer entry on Dec. 31, 2003.

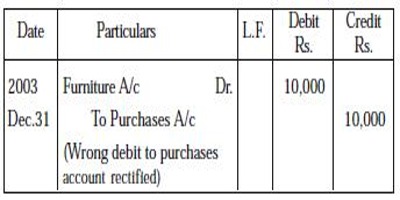

Rectifying Entries: Rectifying entries are passed for rectifying errors which might have committed in the book of accounts.

Example: Purchase of furniture for Rs.10,000 was debited to Purchases Account. Pass rectifying entry on Dec. 31, 2003.