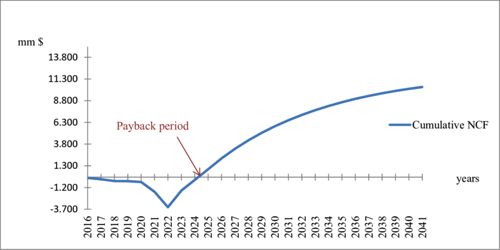

Payback period (PBP) is the number of years it takes for a company to recover its original investment in a project when net cash flow equals zero. In the calculation of the payback period, the cash flows of the project must first be estimated. Normally, it is the time in which the initial cash outflow of an investment is expected to be recovered from the cash inflows generated by the investment. In capital budgeting, the payback period is the selection criteria, or deciding factor, that most businesses rely on to choose among potential capital projects. The calculation used to derive the payback period is called the payback method. The payback period is then a simple calculation.

PBP = years full recovery + unrecovered cost at beginning of last year cash flow in last year.

The payback period is expressed in years and fractions of years. For example, if a company invests $300,000 in a new production line, and the production line then produces a positive cash flow of $100,000 per year, then the payback period is 3.0 years ($300,000 initial investment ÷ $100,000 annual payback).