Single Entry System is an incomplete, incorrect, unscientific and haphazard method of bookkeeping. The name of the system itself shows that the double aspects of business transactions are not recorded. This method records each accounting transaction with a single entry to the accounting records, rather than the enormously more widespread double entry system. This system makes use of Double Entry System partly. It maintains only personal and cash accounts. Real and nominal accounts are not preserves. It is an organism, adopted by certain business houses which, for their convenience and more realistic move toward, reject the strict rules of the double entry system and preserve only the bare necessary records. It is centered on the results of a business that are reported in the income statement. In other words, it is a defective double entry system manipulated to meet the needs of little trading concerns.

According to Kohler “Single Entry System is a system of bookkeeping in which as a rule, only records of cash and personal accounts are maintained. It is always incomplete double entry varying with circumstances”.

Thus, single entry actually refers to an incomplete double entry system or the defective double entry system. It is not based on a dual phase concept. Hence it is incomplete, incorrect, and unscientific.

Therefore, this system does not use nominal and real accounts. The emphasis is on cash and accounts receivable.

Types of Single Entry Accounting System

- Pure Single Entry

This method cannot be used in the practical world since it does not present any information regarding cash or the daily transactions

- Simple Single Entry

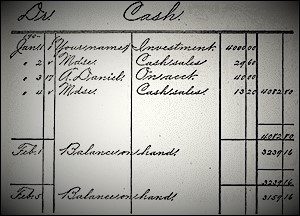

This account is kept on the basis of double entry system but only two accounts are considered, i.e., the individual and the cash account.

- Quasi Single Entry

In this type of accounting apart from the individual and cash accounts, other supplementary accounts are also maintained. The main ones being sales, purchases accounts, and bill books.

Advantages – Main benefits or advantages of single entry system of bookkeeping can be expressed as follows:

- Simple Method of Recording Transaction

It can be maintained simply by the business proprietor. So, this method of book-keeping is easy to preserve and simple to carry out.

- Economical

It is inexpensive because of a limited number of transactions and a limited number of books (only personal account and cash account).

- Time-Saving

It is less time overwhelming because of limited numbers of books and less number of business transactions.

- Easy to Determine Profit and Loss

Profit or loss can be obtained by comparing the ending balance with the beginning of the business for the definite accounting period.

Disadvantages – The following are the important disadvantages of single entry system:

- Unscientific and Unsystematic

This method does not have any set of permanent rules and principles for recording and reporting monetary transactions.

- Incomplete System

This system does not sustain any record of the transactions relating to the nominal account and real account apart from a cash account.

- Does not reflect accurate profit or loss

Under a single entry system, the accurate amount of profit or loss cannot be ascertained because it does not keep the nominal accounts.

- Frauds and Errors

It does not help to confirm the mathematical correctness of the books of accounts. Therefore, there is constantly an opportunity of committing frauds and errors in the books of accounts.

The most considerable problems related to a single entry system include:

- Assets are not tracked, so it is easier for them to be lost or stolen;

- It is impossible to obtain an audit opinion on the financial results of a business using a single entry system;

- Liabilities are not tracked, so you need a separate system for determining when they are due for payment.

This term is used to explain the problems related with the accounts from an unfinished transaction and is commonly called as ‘Preparation of accounts from incomplete records’.