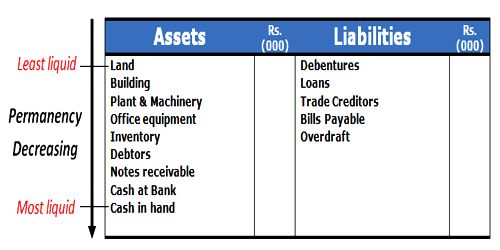

Marshalling of Assets and Liabilities

The term ‘Marshalling’ refers to the order in which the various assets and liabilities are shown in the balance sheet. The assets and liabilities can be shown either in the order of liquidity or in the order of permanence. The process of arranging the balance sheet items (assets and liabilities) in a specific order is called Marshalling of assets and liabilities.

For example (between two creditors), if one has recourse to one source of funds and the other has recourse to two such sources, the funds will be marshaled by the court so that the claims of both creditors are satisfied in the most equitable manner.

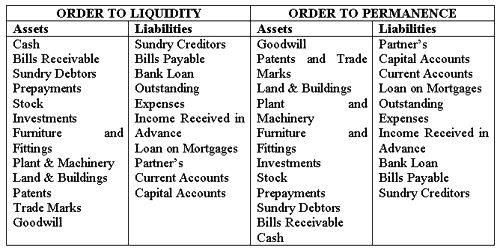

a) In order of liquidity

Liquidity means convertability into cash. Assets will be said to be liquid if it can be converted into cash easily, they are placed at the top of the balance sheet. Liabilities are arranged in the order of their urgency of payment. The most urgent payment to be made is listed at the top of the balance sheet.

b) In order of permanence

This order is exactly the reverse of the above. Assets and liabilities are recorded in the order of their life in the business concern.