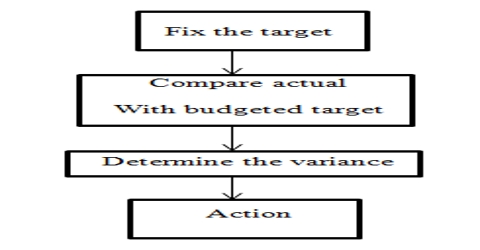

Budgetary control is a method of managerial control in which all operations are designed in advance in the form of budgets and definite results are compared with budgetary principles. This comparison reveals the essential actions to be taken so that organizational objectives are accomplished. Budgetary control refers to how well managers utilize budgets to monitor and control costs and operations in a given accounting period.

A budget is a quantitative statement for a definite future period of time for the purpose of obtaining a given objective. It is also a statement which reflects the policy of that particular period. It will include figures of forecasts both in terms of time and quantities. Managers must remember that budgeting should not be viewed as an end but a means to achieve organizational objectives.

Main objectives of budgetary control are the follows:

- To operate various cost centres and departments with efficiency and economy.

- Elimination of wastes and increase in profitability.

- To anticipate capital expenditure for future.

- Correction of deviations from the established standards.

- Fixation of responsibility of various individuals in the organization.