As the process of business activities alterations, some costs change and some do not. The response of a cost to a big difference in business activity is recognized as cost behavior. Managers must be able to predict the behavior of an particular cost in response to a change specifically business activity. For this purpose, costs are categorized as variable, fixed and mixed costs. This article makes clear these three sorts of costs together with their response to help business activities.

Varied cost:

A cost that changes, altogether dollar amount, with the change in the level of activity is termed variable cost. A typical example of variable cost is direct materials cost. Look at the following example to know how variable cost behaves inside a manufacturing company.

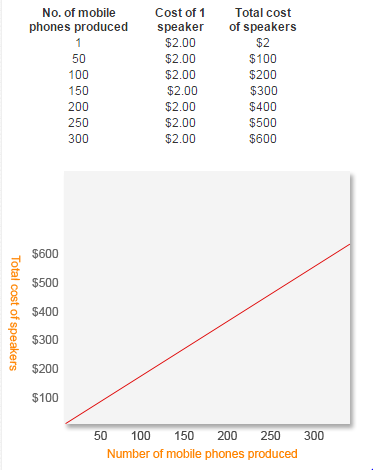

A phone manufacturing company buying speakers from another company at a cost of $2 for every speaker. The speaker is usually a direct materials cost for phone manufacturing company. One speaker is employed to complete a phone. The total and also per unit cost of speakers at various degrees of activity is provided below:

Notice that the total cost of speakers increases as the mobile phones produced are increased but per unit cost remains constant.

Other examples of variable cost include lubricants, sales commission and shipping costs etc.

Fixed cost:

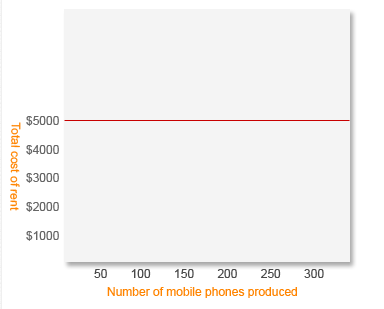

A cost that will not change, in overall, with the adjust in activity is referred to as fixed cost. A typical example of predetermined or fixed cost is rent. In above instance, if mobile cell phone manufacturing company rents a building due to the factory for $5, 000 per month, it will must pay $5, 000 for each and every month even no cell phone is produced during the month. The behavior associated with fixed is shown inside the following figure:

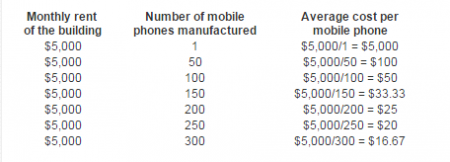

Full fixed cost doesn’t change with your change in task but per device fixed cost changes while using the rise and fall in how much activity. There can be an inverse relationship in between per unit fixed costs and task. If production will increase, per unit fixed cost decreases in case production decreases, each unit fixed cost increases. To understand this point, we incorporate the use of the data through the above example connected with mobile manufacturing business. Consider the following table:

Notice that average fixed cost (computed in the last column) decreases as the production of mobile phones increases. It is an interesting property of fixed cost.

Mixed costs:

A cost which has the characteristics regarding both variable in addition to fixed cost is known as mixed costs. For example, the rental charges of machine might include $500 monthly plus $5 each hour of use. The $500 monthly is a predetermined cost and $5 each hour is a changing cost. Another instance of mixed costs is actually electricity bill. The electricity bill can be divided into 2 parts – (1) series rent and (2) price of units ingested. The line rent just isn’t affected by the consumption of electricity whereas the expense of units consumed varies with all the change in products consumed.