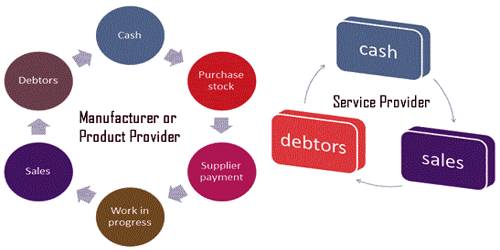

Working Capital Cycle

Working capital is the amount of a company’s current assets minus the number of its current liabilities. Working capital cycle means the cycle of an organization from purchases of raw material to sale or finished goods. Businesses usually undertake to control this cycle by selling inventory swiftly, collecting revenue from customers rapidly, and paying bills gradually, to optimize cash flow. It reflects the ability and efficiency of the organization to manage its short-term liquidity position.

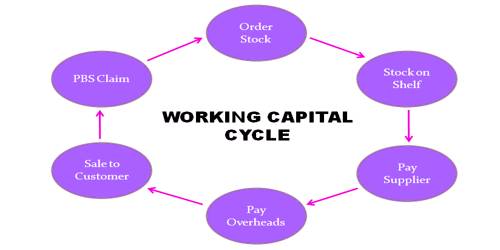

Steps in the Working Capital Cycle – For most companies, the working capital cycle works as follows:

- The company purchases, on credit, materials to manufacture a product,

- The company sells its inventory in 85 days, on average,

- The company receives payment from customers for the products sold in 20 days, on average.

Different factors influencing determining working capital:

- Nature of business;

- Size of the business;

- Production process;

- Production policy;

- Terms of purchase and sale;

- Supply of raw materials;

- Expansion of business;

- The extent of competition;

- Change in technology;

- Dividend policy;

- The rapidity of turnover;

- Depreciation policy;

- Changes in the price level.

Therefore, companies struggle to decrease their working capital cycle by collecting receivables quicker or sometimes stretching accounts payable. So, WCC is a measure of how quickly a business can turn its current assets into cash.