Posting the Opening Entry

The opening entry is conceded to open the books of accounts for the new financial year. The debit or credit balance of an account what we get at the end of the accounting stage is known as the closing balance of that account. This closing balance becomes the opening balance in the subsequent accounting year.

When a business organization shifts from one account period to another accounting period. His assets and liabilities are also shifted. At the beginning of new accounting year, the accountant will pass opening journal entry by writing debit to all assets and credit to all liabilities. The process of posting an opening entry is similar as in the case of a usual journal entry. An account which has a debit balance, the words ‘To balance b/d’ is recorded on the debit side in the details column. An account which has a credit balance, the words “By balance b/d” is recorded in the details column on the credit side. In fact, opening entry is not really posted but the accounts are simply incorporated in the ledger if the ledger is a new one or old.

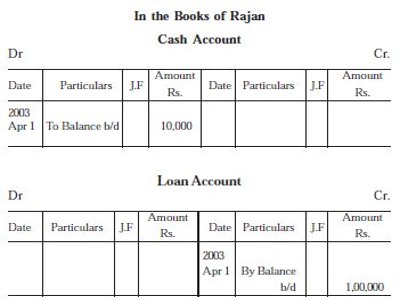

Example: Post the opening entry into the ledger of Rajan as on 1st April 2003, cash in hand Rs. 10,000; Loan Rs. 1,00,000.