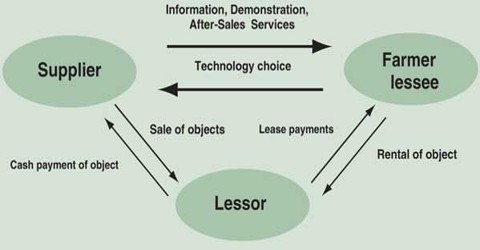

Lease financing is one of the vital sources of intermediate and long-term financing where the holder of an asset gives another person, the right to use that asset against periodical payments. The owner of the asset is known as lessor and the user is called the lessee.

Advantages and Disadvantages of Lease Financing

Advantages

The important merits of lease financing are as follows:

(i) It enables the lessee to acquire the asset with a lower investment;

(ii) Simple documentation makes it easier to finance assets;

(iii) Lease rentals paid by the lessee are deductible for computing taxable profits;

(iv) It provides finance without diluting the ownership or control of the business;

(v) The lease agreement does not affect the debt raising capacity of an enterprise;

(vi) The risk of obsolescence is borne by the lesser. This allows greater flexibility to the lessee to replace the asset.

Disadvantages

The disadvantages of lease financing are given as below:

(i) A lease arrangement may impose certain restrictions on the use of assets. For example, it may not allow the lessee to make any alteration or modification in the asset;

(ii) The normal business operations may be affected in case the lease is not renewed;

(iii) It may result in higher payout obligation in case the equipment is not found useful and the lessee opts for premature termination of the lease agreement;

(iv) The lessee never becomes the owner of the asset. It deprives him of the residual value of the asset.

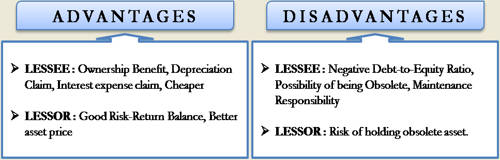

Advantages and Disadvantages of Lease Financing: (In terms of lessor and lessee)

(i) Advantages: Lease financing has the following advantages

(a) To Lessor:

- The Benefit of Tax: As ownership lies with the lessor, a tax benefit is enjoyed by the lessor by way of depreciation in respect of the leased asset.

- High Profitability: The business of leasing is highly profitable since the rate of return based on lease rental, is much higher than the interest payable on financing the asset.

- Recovery of Investment: In the case of the finance lease, the lessor can recover the total investment through lease rentals.

(b) To Lessee:

- Tax Benefits: A company is able to enjoy the tax advantage on lease payments as lease payments can be deducted as a business expense.

- Technical Assistance: Lessee gets some sort of technical support from the lessor in respect of leased-asset.

- Ownership: After the expiry of the primary period, lessor offers the lessee to purchase the assets— by paying a very small sum of money.

(ii) Disadvantages:

(a) To Lessor:

- Unprofitable in Case of Inflation: Lessor gets a fixed amount of lease rental every year and they cannot increase this even if the cost of asset goes up.

- Greater Chance of Damage of Asset: As ownership is not transferred, the lessee uses the asset carelessly and there is a great chance that asset cannot be useable after the expiry of primary period of lease.

(b) To Lessee:

- Ownership: The lessee will not become the owner of the asset at the end of lease agreement unless he decides to purchase it.

- Costly: It is more costly than other sources of financing because lessee has to pay lease rental as well as expenses incidental to the ownership of the asset.