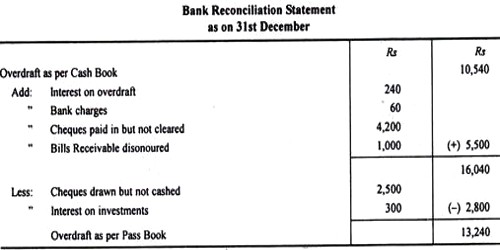

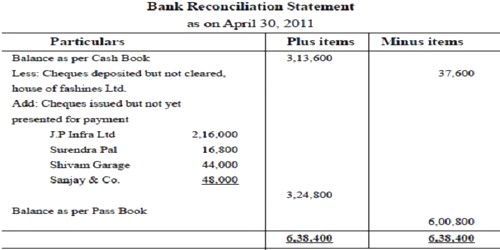

Bank Reconciliation Statement

‘Bank reconciliation statement is a catalog in which a variety of substance that reason a dissimilarity between bank balance as per cash book and pass book on any given date is indicated’.

The balance of the bank column in the double or triple column cash book represents the client’s cash balance at the bank. It should be the similar as shown by his bank pass book on any particular day. For every entry made in the cash book if there is a corresponding entry in the pass book (maintained by the banker) or vice versa, the bank balance will be similar in both the books.

However, it must be noted that the cash book and the pass book are maintained by two dissimilar parties and therefore it is not assured that access in one book will constantly have a consequent entry in the other. Usually, entries in the cash book should tally (agree) with those in the pass book and the balances shown by both the books should be similar. But in practice, the balances usually be different. In case of dissimilarity in the balance of the cash book and the pass book, the need for preparing Bank Reconciliation Statement arises.